#Investment Thesis

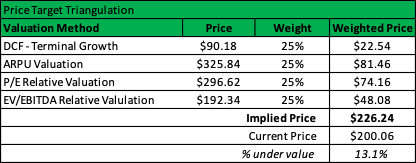

Our analysis recommends a buy rating for Meta Platforms Inc. with a target price of 226.24, reflecting a 13.1% undervaluation based on current market prices. This recommendation is anchored on several key factors:

- Regulatory Challenges: While regulatory changes, particularly around data privacy, pose medium-term risks, Meta's proactive investments in compliance and innovation position it to navigate these hurdles effectively.

- Metaverse Potential: The Metaverse initiative represents a transformative growth opportunity. By integrating social media, virtual reality, and digital commerce, Meta aims to create a unified platform that could redefine digital interaction and unlock new revenue streams.

#Valuation

Our valuation approach employs multiple financial models to provide a comprehensive and precise assessment of Meta Platforms Inc. (Meta). These models include Discounted Cash Flow (DCF), Average Revenue Per User (ARPU), Price/Earnings (P/E) relative valuation, and EV/EBITDA. By triangulating these methods, we ensure a robust and nuanced valuation, highlighting Meta's potential for growth amidst industry challenges. The company operates through two primary segments:

- Family of Apps (FoA): This includes Facebook, Instagram, WhatsApp, and Messenger. As of Q4 FY 2021, FoA generated 97% of Meta’s revenue, amounting to $32.8 billion, with an operating income of $15.9 billion, reflecting a 6.8% year-over-year growth.

- Reality Labs (RL): This segment focuses on augmented and virtual reality, including Oculus. In Q4 FY 2021, RL reported $877 million in revenue, a 22% year-over-year increase, but also an operating loss of $3 billion.

#DCF – Terminal Growth

Meta's revenue primarily comes from advertising. The company provides free tools and services to billions of users and monetizes this large user base by selling advertisement space to businesses and leveraging user data. Meta prioritizes increasing Daily Active Users (DAUs) to maximize ad revenue. Innovative features like Instagram Reels and Stories are introduced to retain user engagement and compete with platforms like TikTok and Snapchat.

- Current Market Price of Meta is $200 per share, while the DCF model implies a value of $107 per share, suggesting the stock is overvalued by approximately 47%

- Enterprise Value (EV) is $567,718 million, accounting for long-term debt and cash equivalents

- The Cost of Equity is calculated at 9.35%, influenced by a risk-free rate of 2.03%, market risk premium of 5.8%, and an adjusted beta of 1.26

- The WACC is 9.3%, indicating the overall discount rate used for future cash flows

#ARPU – Average Revenue Per User

The valuation based on ARPU uses a regression of how price and revenue correlate over the past five years. Then the projected revenue, again assuming slowing growth in the number of users and ARPU, is plugged in and the resulting price is $325.84.

- Regression analysis on historical price and revenue data.

- Projected revenue growth at a slower pace.

- Implied price: $325.84.

- Highlights effective monetization of user base.

#P/E Relative Valuation

- Growth premiums aligned with 9% WACC.

- Bear: Average of current and median EPS of comparables (excluding Alphabet), slightly lower P/E.

- Base: Based on Meta’s current EPS.

- Bull: Average EPS and P/E of comparables.

#EV/EBITDA Relative Valuation

- Aligned with current market price.

- Similar growth assumptions as other models.

- Reflects stable operational performance and strategic investments.

#Tools and Skills Used

- Financial Modeling: Expertise in creating and analyzing Discounted Cash Flow (DCF), Average Revenue Per User (ARPU), Price/Earnings (P/E), and EV/EBITDA models to derive accurate valuations.

- Data Analysis: Proficient in using regression analysis to project revenue growth and user base trends.

- Market Research: Conducted thorough market and competitive analysis to understand Meta's positioning and growth potential.

- Strategic Planning: Evaluated and articulated Meta’s strategic initiatives, including Metaverse investments and R&D spending.

- Report Writing: Compiled detailed investment reports with clear, data-driven recommendations.

- Presentation Skills: Created compelling visualizations and summaries to communicate findings effectively.

- Software Proficiency: Utilized financial software and tools for data analysis, modeling, and visualization.

- Project Management: Managed the project timeline, ensuring thorough analysis and timely completion of the report.

#Conclusion

- Target Price: $226.24 (13.1% upside).

- Drivers: Strategic growth initiatives, robust user monetization, effective regulatory management.

- Approach: Comprehensive and multi-faceted analysis, demonstrating Meta’s potential in the digital landscape.

- Robust Valuation: Utilizing DCF, ARPU, P/E, and EV/EBITDA models, our comprehensive valuation approach underscores Meta's strong potential in the evolving digital landscape.

#Appendix: